Share

Executive Summary:

While the US early childhood education market continues to present strong growth opportunities, market participants face several challenges that can limit scalability. Success will depend on clearly defining target customers and markets, aligning go-to-market strategies with purchasing behaviors, and building scalable operational capabilities. Organizations that combine strategic focus with disciplined execution will be best positioned to capture long-term growth and market share.

The US early childhood education (ECE) market remains an attractive growth arena for operators, product and service providers, and investors. Demand for quality care is durable, parent expectations continue to rise, and the market remains highly fragmented. However, scalability is a challenge: labor availability and cost, local market dynamics, and varied customer needs all create execution risk.

Against this

backdrop, the next phase of growth in the ECE landscape will favor organizations that combine strategic focus with operational discipline. The strongest platforms will define where they have the greatest right to win, align their go-to-market model with how customers buy, and build a repeatable playbook that supports scalable execution and long-term value creation.

The ECE Landscape: Market Context

A Large Market with Meaningful Headroom for Growth

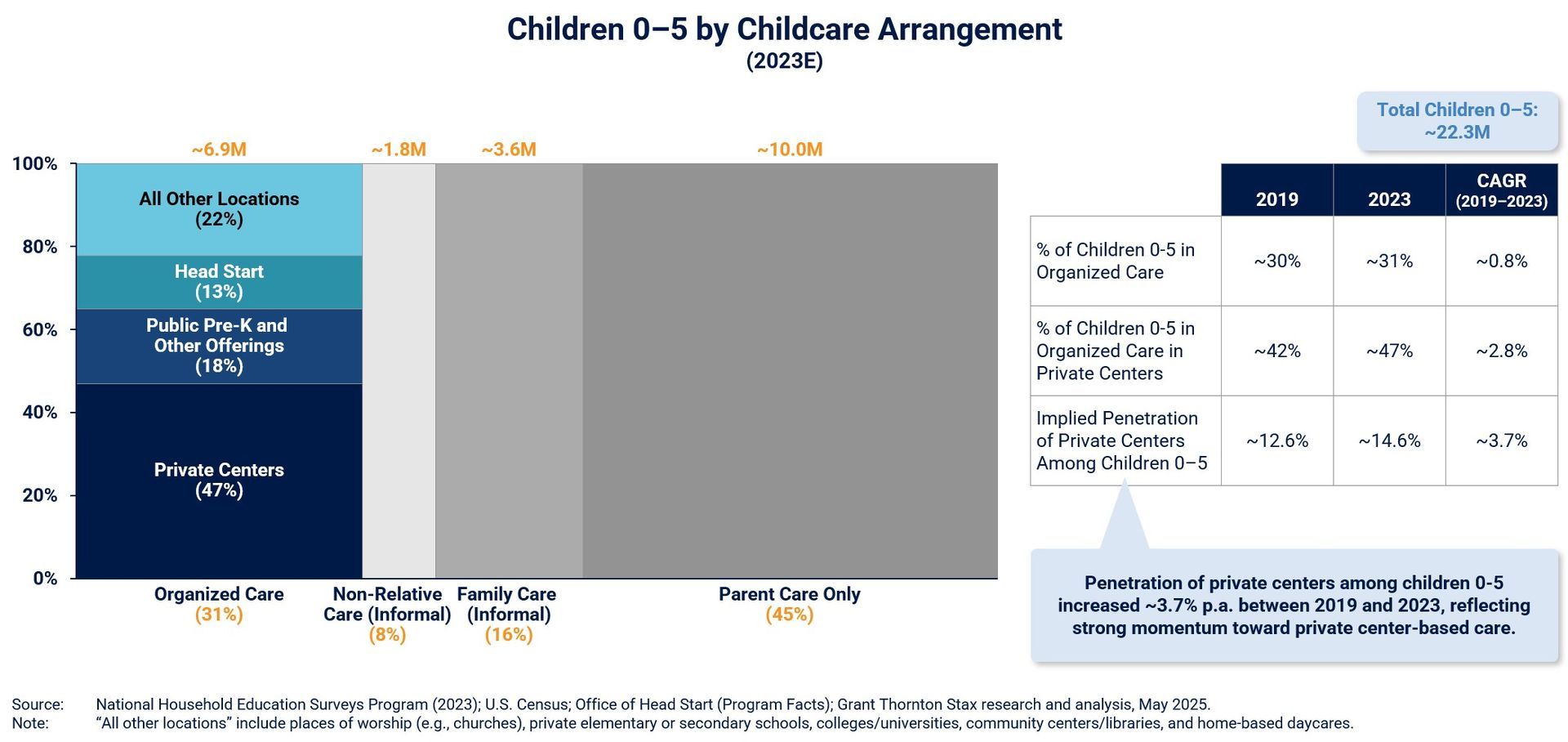

Early childhood education remains underpenetrated, with less than one-third of children ages 0–5 enrolled in organized childcare today. Private centers have gained share in recent years and now serve roughly half of 0–5 children in organized care, reflecting a secular shift toward structured and professionalized care environments (Figure 1).

Figure 1:

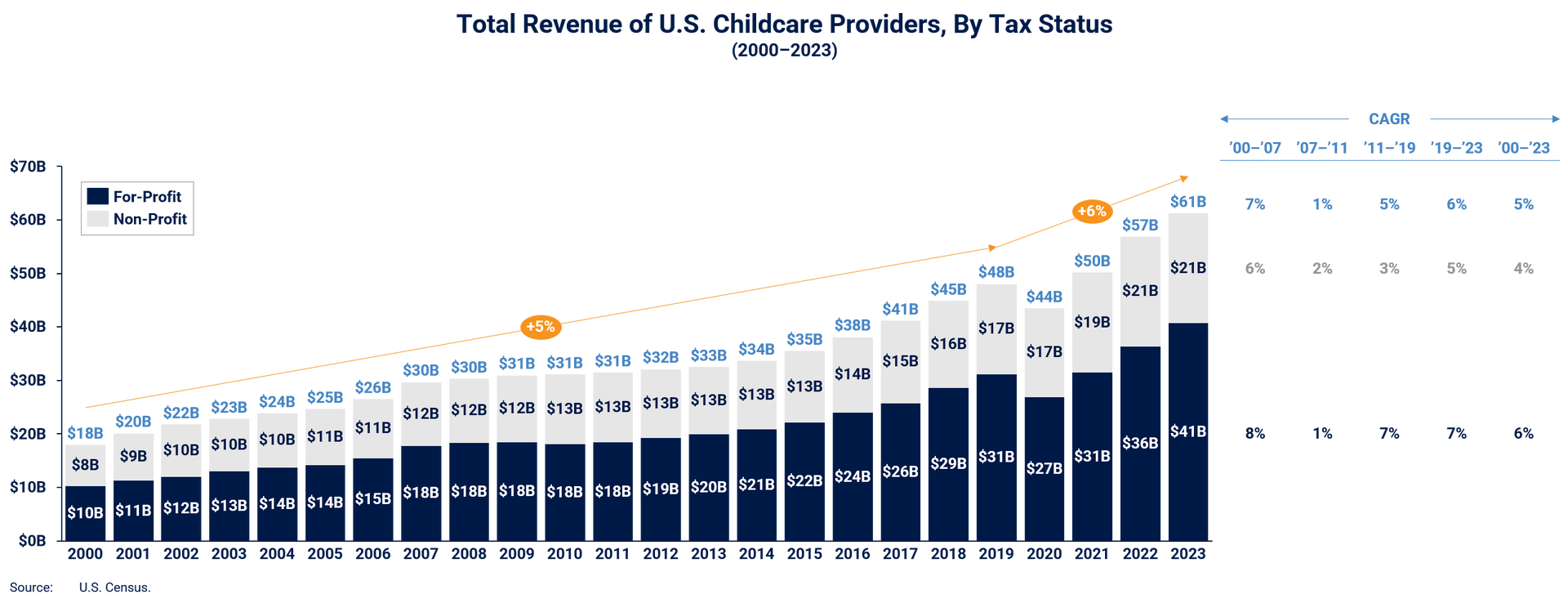

In addition to its large size, the private childcare market also has an attractive growth profile, with provider revenues increasing consistently for more than two decades (Figure 2). Looking ahead, growth is expected to be driven less by expansion in the 0–5 population—which the US Census projects will remain largely flat into 2030—and more by continued penetration of private centers and tuition increases.

Figure 2:

Parent Expectations are Shifting

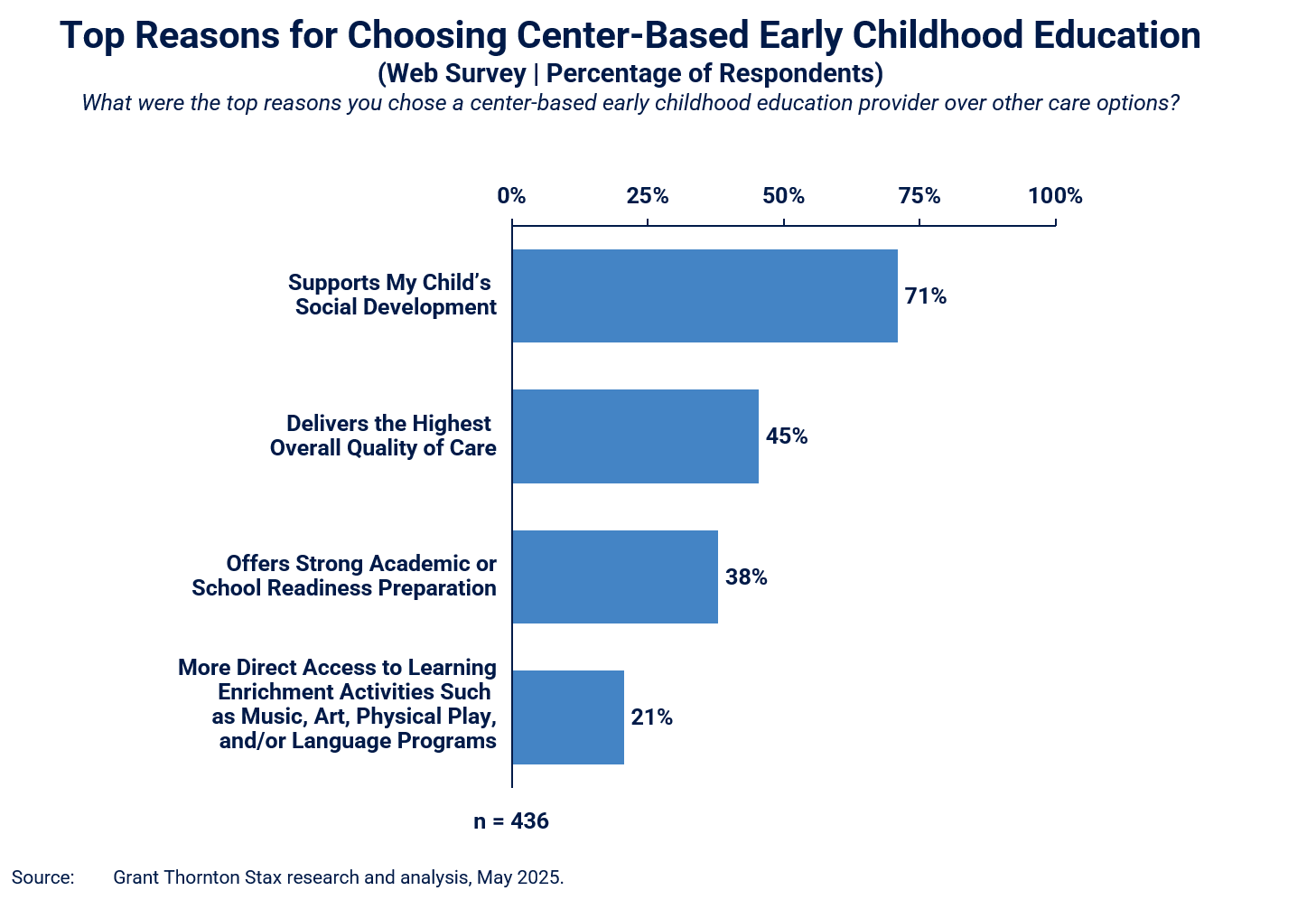

Parents no longer evaluate early childhood education solely through the lens of basic care coverage and convenience. Increasingly, they are seeking developmental, educational, and social benefits that help children build confidence and kindergarten readiness.

Across the market, parents are placing greater emphasis on social development, quality of care, academic readiness, and enrichment activities such as music, art, language, physical play, and STEM-oriented programming. These preferences align strongly with the value proposition of private centers, particularly those that provide transparency into the child experience and build trust with families (Figure 3).

Figure 3:

Additionally, affordability remains an important consideration as childcare is a meaningful household expense. However, parents tend to view childcare as essential which supports demand resilience through income declines and economic cycles—especially among dual-income and higher-income households.

For ECE providers, the implication is clear: positioning matters. Operators that can credibly deliver safety, reliability, education, and enrichment are best positioned to sustain pricing power and capture share.

Fragmentation Creates Opportunity, but Execution Matters

Despite the presence of scaled national operators, the US ECE market remains highly fragmented. National brands account for less than 10% of total centers, leaving substantial runway for consolidation through buy-and-build strategies.

While this fragmentation is attractive, it also introduces complexity. Brands vary widely in terms of target parent demographic, price point, curriculum model, and service level, and strategies that work in one market do not necessarily translate to another.

For operators and their investors, expansion must be grounded in rigorous market screening and selection, prioritizing geographies with large and growing populations of 0–5 children, strong labor force participation rates, childcare seat shortages, and favorable regulatory dynamics—alongside brand-specific success factors. Leading platforms pursue density in selected markets rather than dispersion, intentionally clustering locations to build brand awareness, optimize staffing, enhance operational performance, and create powerful parent referral loops.

Labor Availability Remains the Critical Bottleneck

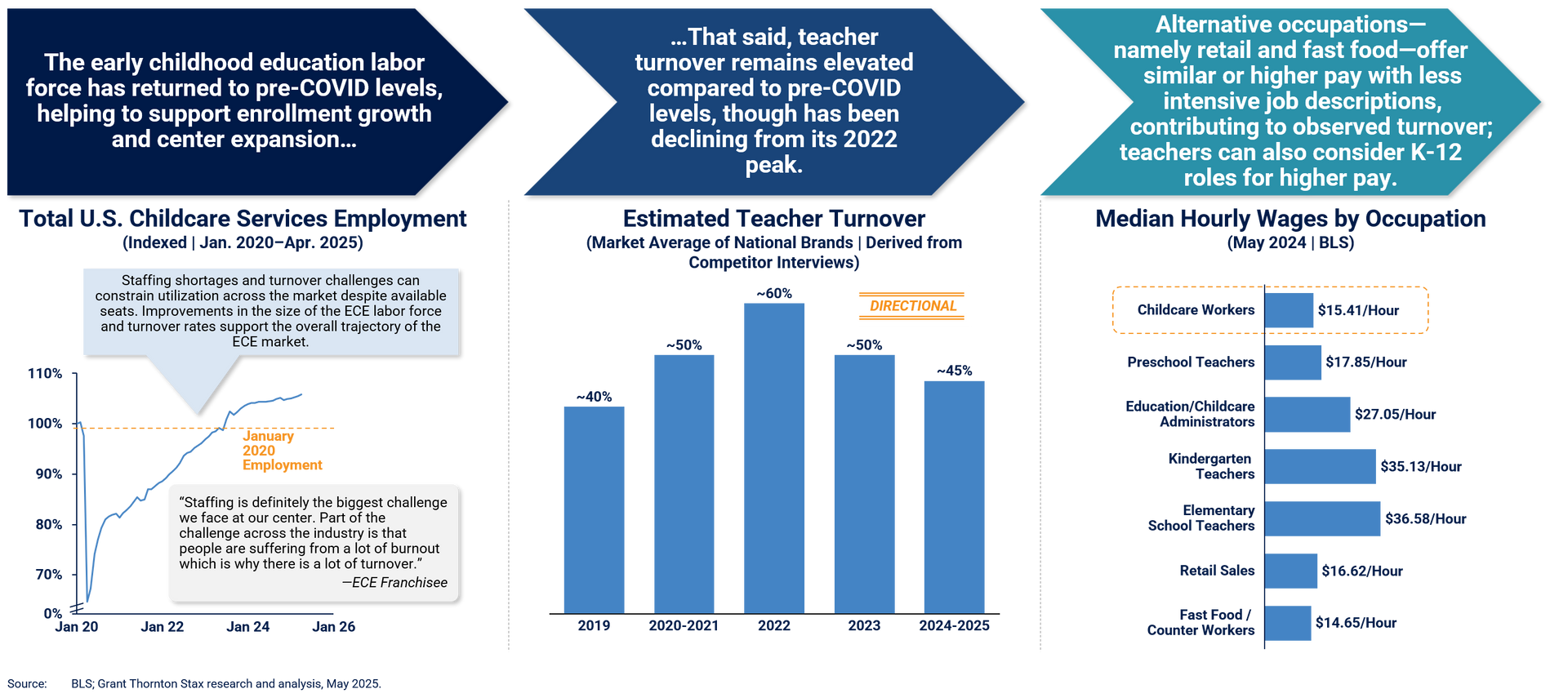

The strong demand-side story in ECE is tempered by a persistent supply-side constraint: labor. While the childcare labor force has recovered to pre-Covid levels, turnover remains elevated, and competition for talent persists. Childcare wages are often lower than those in alternative fields such as retail, food service, and K-12 education despite the work requiring significant responsibility and energy, contributing to observed turnover (Figure 4).

Figure 4:

An effective operating model is essential to mitigating staffing shortages, which can limit capacity utilization, pressure service quality, and constrain both same-center and new-center growth—even when parent demand remains strong. Leading platforms have responded by building comprehensive talent engines spanning recruiting, onboarding, compensation and benefits, training, and career development pathways, turning workforce attraction and retention into a competitive advantage rather than a challenge.

The Three-Step Expansion Playbook for ECE Market Participants

Current market dynamics and structural characteristics of the ECE landscape create both opportunities and complexities for operators and the product and service providers that serve them.

To drive sustainable growth, organizations must understand where to play, how to engage customers, and how to translate strategy into action. These priorities can be distilled into a three-step expansion playbook:

Step One: Define Where to Play

The first requirement for growth is clarity on where to play.

In ECE, this means precisely defining the ideal customer profile and target market. For center operators, customer segmentation should reflect affluence, funding source (self-funded, employer-sponsored, or subsidy-supported), and care preferences, with prioritization driven by strategic fit. For product and service providers, effective segmentation requires distinguishing centers by brand (national, regional, or independent) and delivery model, focusing on segments where needs and willingness to pay align with the value proposition and where competitive positioning is differentiated and defensible.

Step Two: Align the Go-to-Market Model to the Buying Journey

The second requirement is aligning the go-to-market model with the buying journey.

Purchasing processes in ECE vary significantly by offering and customer type. Parents selecting a childcare center weigh factors such as trust, proximity, perceived quality, and price-to-value. The decision is highly personal and requires providers to build confidence throughout the family journey—from initial awareness and consideration through enrollment. Centers evaluating curriculum, software, supplies, staffing solutions, and facilities services often involve both center- and network-level stakeholders assessing operational impact, cost, scalability, and compliance.

Effective go-to-market design should reflect these distinct buying dynamics and be tailored to the target market and best-fit customer. For both operators and their vendors, this requires mapping the most influential channels, value drivers, and purchasing criteria (e.g., quality, child outcomes, price, ongoing support) and translating these elements into a coherent commercial strategy that effectively generates and converts demand.

Childcare providers typically rely on a combination of digital marketing, referral networks, employer relationships, and community partnerships to generate awareness and attract prospective families. However, demand generation represents only the first stage of the enrollment journey: sustainable enrollment growth requires a strong conversion engine that moves families from inquiry to tour to enrollment. Providers must create effective pathways for capturing inquiries, responding quickly, building relationships, delivering compelling tour experiences, addressing parent decision criteria, and reducing administrative friction during enrollment. Key conversion drivers include transparent and timely communication, strong parent testimonials, demonstrations of quality and safety, clear explanations of educational programs, and a seamless enrollment process. Leading operators measure performance across the enrollment funnel, including inquiry volume, inquiry-to-tour conversion, tour attendance, and tour-to-enrollment conversion.

For childcare product and service providers, go-to-market models must similarly align with customer buying realities. Large multi-site or strategic accounts often require direct sales approaches involving account management, demonstrations, and consultative selling. Relationship-driven segments may be best served through field representatives or dealer-led models, while distributor-enabled approaches can provide efficient access to the long tail of independent centers.

Step Three: Turn Strategy into Execution

The third requirement is translating strategy into execution.

A strong roadmap scopes and prioritizes go-to-market initiatives based on impact, feasibility, investment, and risk. Each initiative should be directly linked to a defined growth objective: for childcare operators, this may include accelerating lead conversion, increasing capacity utilization, or strengthening parent retention, and for product and service providers, this may include enhancing demand generation, improving channel productivity, or deepening penetration within existing accounts.

Leading market participants treat initiatives not as isolated activities, but as interconnected components of a cohesive commercial system. Marketing, sales, and customer success work in concert to reinforce the value proposition, improve customer acquisition and retention, and maximize customer lifetime value.

Grant Thornton Stax Perspective

The opportunities in early childhood education are substantial but realizing them will require more than simply participating in a growing market. As the industry evolves, market leadership will not come from pursuing growth indiscriminately, but from making deliberate choices about where to play, aligning go-to-market approaches with how customers buy, and building the capabilities needed to execute consistently at scale.

Organizations that outperform—whether serving families directly or enabling the providers that do—will be those that bring clarity to where they can create the most value and discipline to how they deliver. Success starts with a deep understanding of the customer and is realized by translating those insights into focused actions and long-term growth.

To learn more about our Education and Value Creation expertise, visit our Insights page or contact us directly.

Read More