Share

Executive Summary:

The crane services sector is entering a new phase of investor attention as a result of several factors: cranes being non-discretionary to industrial operations, structurally high outsourcing penetration, and built-in insulation from typical industrial downturns. In addition, the industry remains highly fragmented, creating meaningful platform-building opportunity.

A Structurally Outsourced, Mission-Critical Market

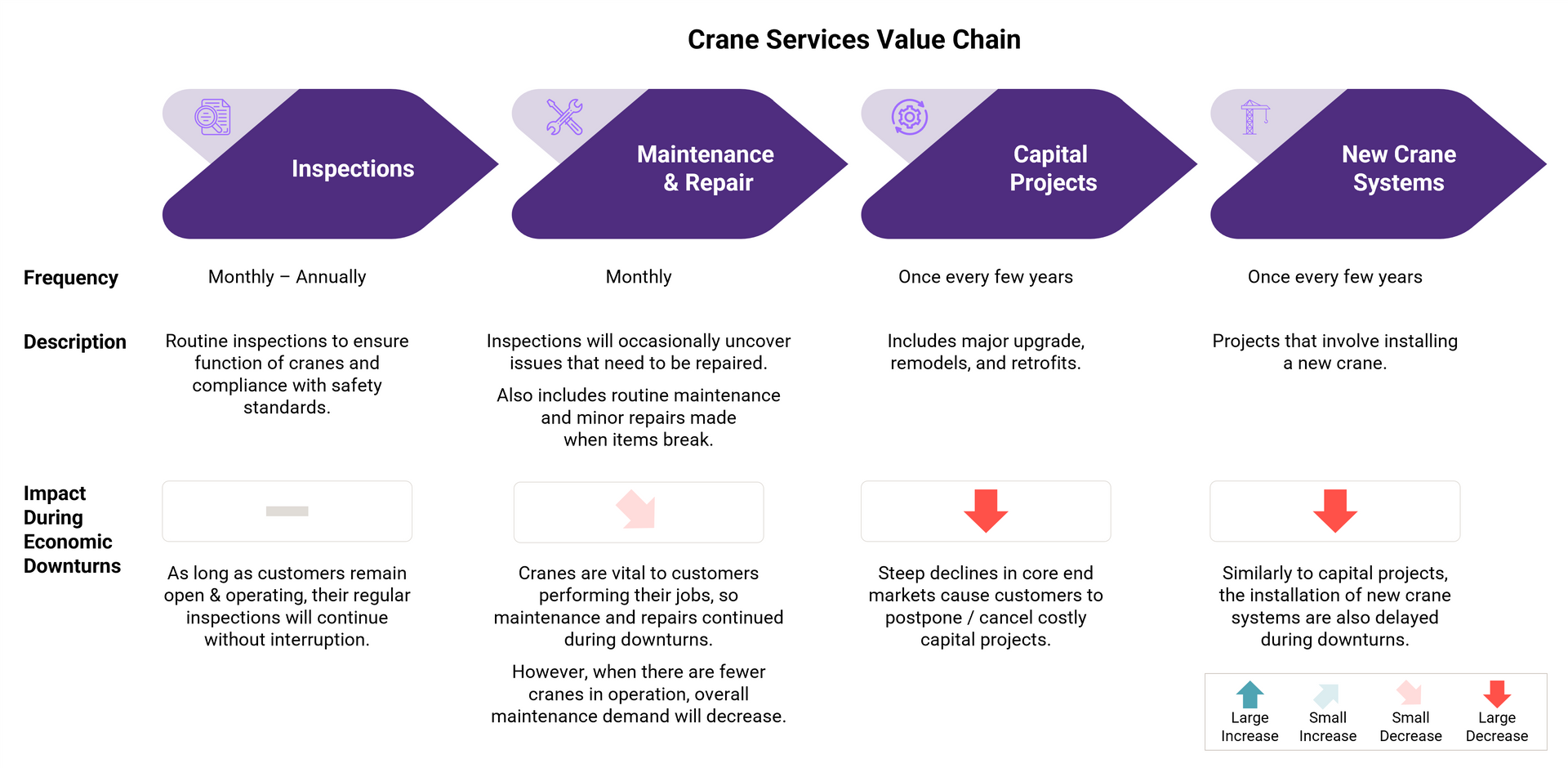

Overhead and mobile cranes are critical to plant operations. When a crane becomes inoperable, whether due to maintenance, mechanical issues, or other disruptions, production can slow or stop altogether, often at a cost of millions of dollars per day in lost output.

Most asset owners do not service their own cranes. The economics of carrying high-cost, low-utilization equipment, combined with the specialized labor and safety expertise required, have made third-party service the default operating model. As a result, the crane services market is already highly outsourced. The structural drivers of that outsourcing (capital intensity, technical complexity, safety liability) are intensifying.

Where Is the Demand Coming From?

Crane services demand is driven by several macro tailwinds that should sustain growth for the foreseeable future:

- Industrial reshoring and manufacturing capex: New domestic capacity in semiconductors, EV/battery, automotive, aerospace, and heavy industry is generating both installation demand (new equipment) and recurring service demand (inspections, repairs, modernization).

- Infrastructure investment: Federal infrastructure spending is driving sustained activity in ports, energy, and transportation; each of which is crane-dependent.

- End-market durability: Cranes serve a variety of end-markets that experience cyclicality, though crane services are anchored by non-discretionary uptime requirements.

- Aging installed base. A large portion of the US overhead crane base is well beyond its design life, sustaining inspection, repair, modernization, and replacement demand independent of new capacity additions.

Recession Resilience: Why This Cycle May Look Different

Machinery maintenance and repair spend has historically declined modestly in prior recessions, reflecting the non-discretionary nature of mission-critical equipment upkeep. Future downturns may offer even greater insulation, for two reasons:

- The skilled labor shortage is making in-housing harder: As internal capability erodes, outsourcing becomes the default.

- Cranes are increasingly part of the labor solution: Operators are adding cranes to reduce headcount requirements, expanding the installed base.

Together, these forces suggest crane services demand should hold up better in the next downturn than in prior cycles.

A Fragmented Competitive Landscape Being Reshaped by Technology

The market is highly fragmented across national, regional, and local providers. National players win on capital projects and multi-site accounts, but struggle with consistent local service. Likewise, local players win on responsiveness and relationships but lack capacity for large-scale work. Regional players operate in between.

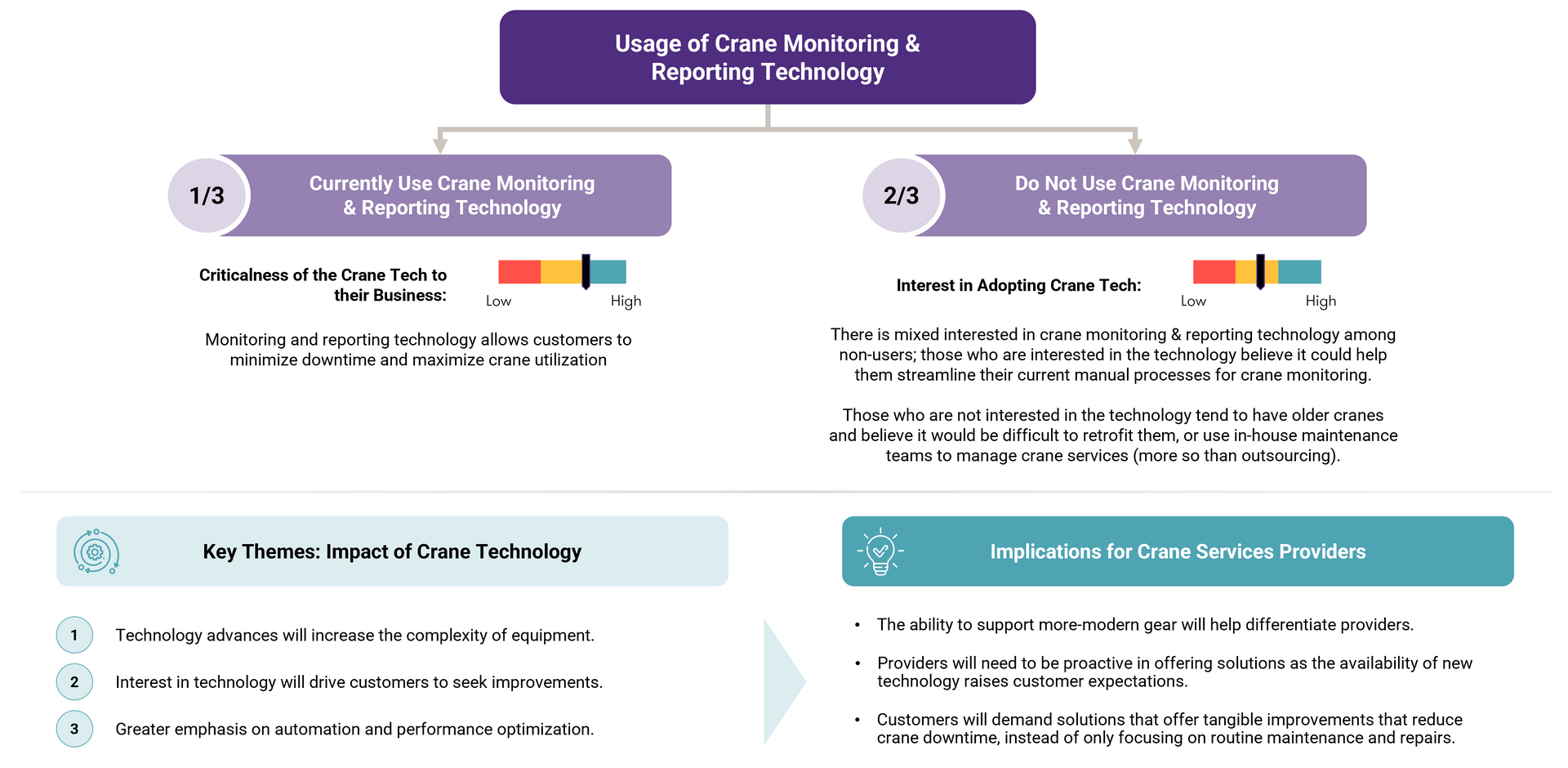

Technology is now reshaping this dynamic. Roughly one-third of customers use crane monitoring and reporting technology, but the majority expect technology adoption to materially impact how crane services are delivered, shifting demand from reactive emergency repairs toward proactive, data-enabled maintenance and performance optimization. Customers increasingly expect providers to anticipate issues and optimize utilization.

Where Private Equity Value Is Being Created

Our view at Grant Thornton Stax, informed by multiple recent engagements across the sector, is that value is driven by:

- A durable, recurring service core tied to mission-critical installed bases.

- Local density combined with regional or national scale, delivering responsiveness customers are demanding alongside operating leverage and multi-site coverage.

- Credible adjacency expansion into rigging, machinery moving, millwrighting, hoist and lift services, and broader plant maintenance, extending wallet share and the addressable market story at exit.

- A defensible technology posture. Monitoring, predictive diagnostics, and data-enabled service offerings are increasingly differentiating providers.

Risks Investors Should Consider

A balanced view requires acknowledging where this sector can disappoint:

- End-market cyclicality: Exposure to steel, energy, and heavy manufacturing introduces cyclical risk. Recessionary periods compress capital project activity, even as inspection and emergency repair work proves more resilient.

- Labor availability: Skilled crane technicians are scarce. Platforms that have invested in training infrastructure and certification programs hold a defensible advantage.

- Competition for add-ons: As more sponsors enter the space, multiples for quality regional operators are rising.

- Technology disruption: IoT-enabled diagnostics and predictive maintenance tools are beginning to reshape how service work is scoped and delivered, creating opportunity for tech-forward providers and risk for those that fail to adapt.

Strategic Implications: Where to Focus, What to Watch

The crane services sector is a structurally outsourced, mission-critical, recurring-revenue business with durable demand tailwinds, meaningful recession insulation, a clear white space in the competitive landscape, and substantial platform-building opportunity. These qualities should continue to attract significant private equity capital.

For investors, several questions should anchor the diligence:

- How durable is the recurring service revenue base?

- What is the platform's technology posture, and how is it monetizing monitoring and reporting capabilities?

- Is the revenue mix shifting from reactive emergency work toward proactive, technology-enabled maintenance?

- How credible is the adjacency expansion thesis, and is the operational capability in place to execute?

To learn more about our Industrial services expertise, visit our Insights page or contact us directly.

Read More