Share

Executive Summary:

Grant Thornton Stax Partner Chen Liu demonstrates our AI risk framework within a specific vertical software segment (GovTech ERPs). These platforms benefit from strong technical and commercial moats, including deep domain expertise, complex integrations, high switching costs, and risk-averse customers, all of which limit competitive disruption from AI-native or horizontal entrants. While AI may pressure certain elements, such as seat-based pricing models or adjacent features like analytics and workflow tools, the core system-of-record functionality remains durable and unlikely to be displaced. Overall, evaluating AI risk requires distinguishing between core resilience and peripheral exposure, with outcomes varying significantly based on a product’s role, complexity, and market dynamics.

A growing body of commentary on AI’s impact on software businesses spans a wide spectrum, from warnings of the impending “SaaS-pocalypse” to views that “the whole thing is way overblown.” To make the rhetoric more tangible, Grant Thornton Stax sought to apply and showcase a basic AI risk framework within a specific vertical software segment.

For our example, let’s think about a GovTech ERP (financial software) that sells into small and mid-sized state and local governments (SLGs). Intuitively, a GovTech ERP feels relatively insulated from AI risk (i.e., sticky, mission-critical, high switching costs) but let’s validate this thinking in a more structured manner.

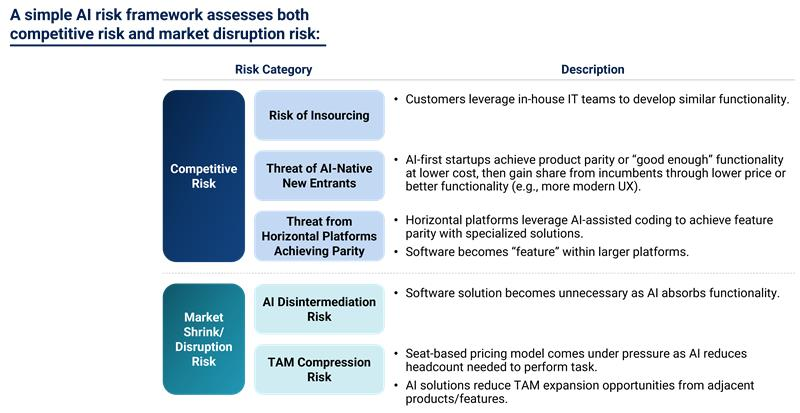

This exercise uses a two-part framework: Competitive replication risk (e.g., from AI-native entrants, horizontal platforms achieving feature parity) and market shrink risk (e.g., AI reducing the underlying need for the product).

Competitive Replication Risk

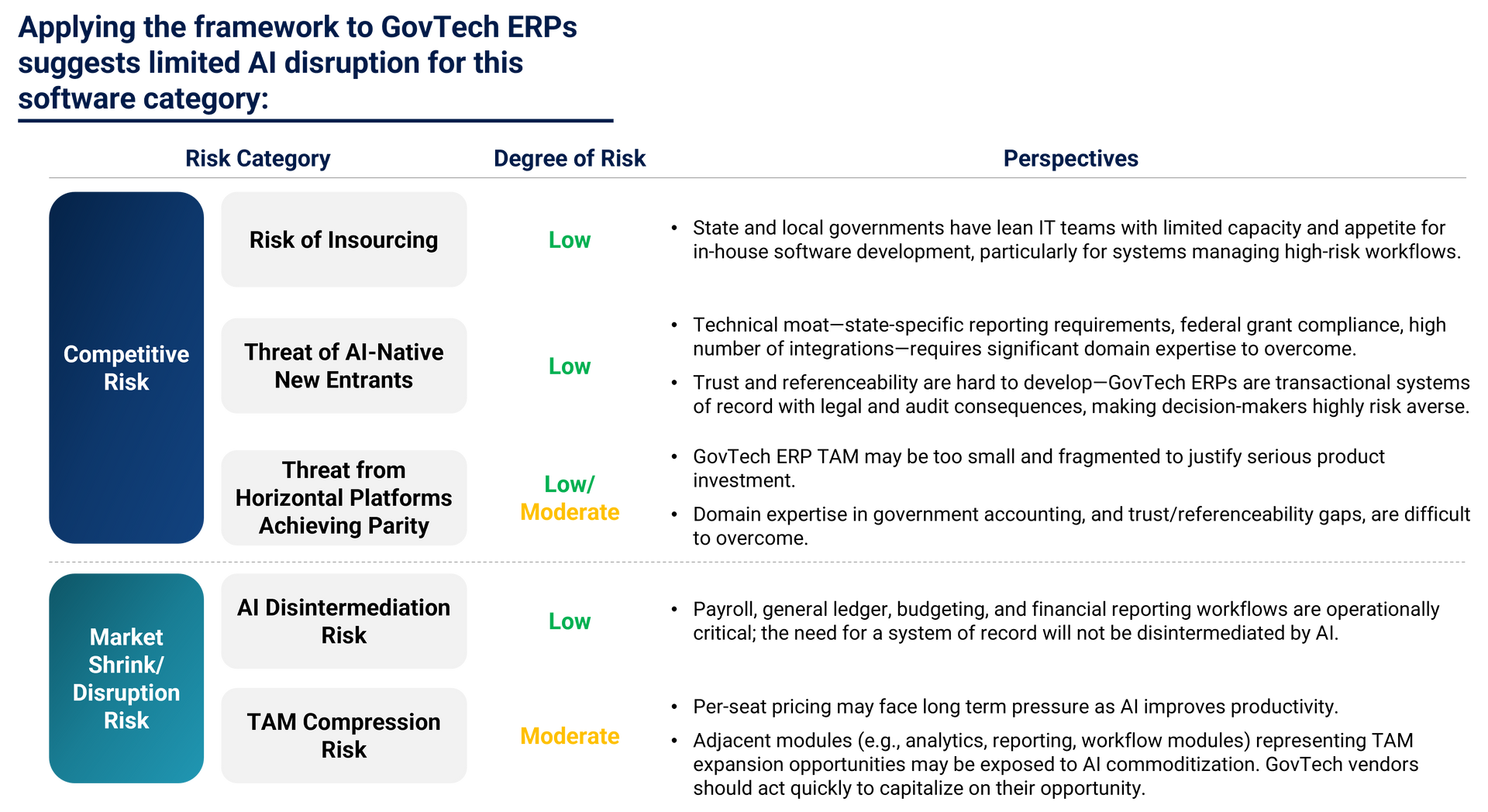

Insourcing: Not a real risk for GovTech ERPs

The insourcing risk for small to mid-sized state and local governments is close to zero. These organizations typically have limited IT teams and appetite for the operational risk of developing their own ERP solutions that manage critical payroll and budgeting workflows.

AI-native new entrants: Real question, but lower risk than it might appear

AI-assisted coding can reduce the cost and time to build ERP-like functionality, and some incumbent GovTech ERPs have a reputation for somewhat dated interfaces and clunky UX. The case for a modern new entrant can be made.

That said, several technical barriers exist that new entrants would find challenging to overcome.

- Domain expertise encoded in product: GovTech ERPs must comply with a wide range of government-specific requirements—GASB accounting standards, state specific reporting mandates, federal grant compliance frameworks, etc. Coding these requirements correctly requires deep domain knowledge that accumulates over years of working across different types of government entities.

- Integration depth: GovTech ERPs are also typically integrated with many other software solutions, including state reporting portals, HR platforms, municipal software, etc., and those integrations are built using APIs and data structures that require meaningful time to develop.

- Edge case hardening: Lastly, new entrants would have a hard time managing edge cases; LLMs are probabilistic; business logic is deterministic; the long tail of jurisdiction-specific requirements cannot be easily replicated.

The commercial moat for GovTech ERPs compounds the technical one. GovTech ERPs are transactional systems of record—they don’t just facilitate workflows, they execute them, creating financial records with legal and audit consequences. A missed payroll or miscoded journal entry is not just a bad user experience; it can mean an audit finding or compliance violation. This makes government buyers highly risk-averse in vendor selection. SLG decision-makers buy from vendors with documented track records working with similar government entities, and that credibility takes years to build.

High switching costs are an additional barrier. The challenge is not just migrating data and training end users, but also customized configuration (e.g., chart of accounts structures, fund accounting workflows, integrations with state and federal reporting systems). Switching may be easier for smaller SLGs than for large cities, but they remain substantial relative to the potential gain from a more modern solution.

Horizontal vendors: similar barriers to AI-native entrants

The risk from large horizontal players (e.g., Microsoft, Oracle) to “catch up” to the needs of the state and local government customer base is also likely low. They lack the domain expertise and established track record required to succeed in this segment, and the fragmented, relatively smaller SLG ERP market may not justify significant product investment.

Market Shrink Risk

The core ERP is not going anywhere

ERPs are systems of record for government entities. Payroll, general ledger, budgeting, and financial reporting systems are legally binding processes that require auditable and defensible records that cannot be disrupted / eliminated by AI.

Pricing model disruption: Slow-moving but potentially real

Most GovTech ERPs are priced on a per-seat basis, which faces pressure as AI increases productivity and allows fewer users to manage the same workload. However, SLG workforce dynamics are slow-moving. Civil service protections and the political sensitivity surrounding layoffs at the state and local level suggest that AI-driven headcount reductions are more likely to unfold over the medium to long term.

Adjacent market expansion: Opportunity is there, but risk exists for slow movers

Many GovTech ERP vendors have expanded into new areas including analytics dashboards, reporting tools, document management, and workflow automation. These are the point-solution capabilities that AI is most likely to commoditize in the near term.

GovTech ERP vendors have a natural right to win here: they own the data, the customer relationship, and the credibility. However, vendors that move too slowly risk SLGs adopting AI-native point solutions / capabilities from other tools already embedded in their software ecosystem. In these cases, the core may remain resilient while the growth opportunity somewhat softens.

The Takeaway

As expected, the GovTech ERP example lands in a relatively comfortable place. AI is unlikely to result in competitive displacement, and the core functionality is durable.

However, this quick exercise highlights a useful framework on how to consider the various risks that AI can pose, as well as potential mitigants from both a technical and commercial angle. Applying this lens to other types of GovTech software, the key question becomes which elements of the ERP moat persist—and which do not.

As a category, GovTech software benefits from structural advantages that apply broadly: low insourcing risk, limited appetite for displacement from horizontal players, and a risk-averse decision-maker that prioritizes government referencability. On the other hand, GovTech solutions that are workflow-driven—requiring less encoded domain expertise, involving fewer integrations across the broader GovTech stack, and playing a less central role in executing critical government workflows—may be more exposed.

To learn more about

GovTech and our broader

Software & Technology expertise, visit our

Insights page our

click here to contact us directly.

Read More