Share

Executive Summary:

GovTech remains an attractive investment category due to its resilient demand, high switching costs, and fragmented vendor landscape, with modernization trends further accelerating adoption. The market is complex and highly localized, shaped by siloed decision-making, regulatory requirements, and a strong emphasis on trust and proven track records. Structural tailwinds—including rising citizen expectations, regulatory pressures, and resource constraints—are driving continued demand for digital solutions across both internal operations and public service delivery. While relatively insulated from near-term AI disruption, the sector presents opportunities for investors through targeted consolidation and platform-building strategies, particularly in mission-critical and fragmented sub-verticals. Success, however, depends on aligning products with real workflow needs and navigating geographic and operational nuances to create cohesive, integrated solutions.

GovTech has historically been an attractive investment category, supported by resilient end markets, a fragmented vendor landscape, and high switching costs. Recently, the sector has become increasingly more compelling as modernization trends accelerate software adoption and the category remains relatively insulated from near-term AI disruption. At the same time, navigating the market may be difficult due to localized requirements, siloed decision-making, and complex procurement dynamics.

At Grant Thornton Stax, we provide an overview of the GovTech ecosystem for state and local governments, highlight key market trends, and outline where we see some compelling investment themes.

Overview of the State and Local GovTech Landscape

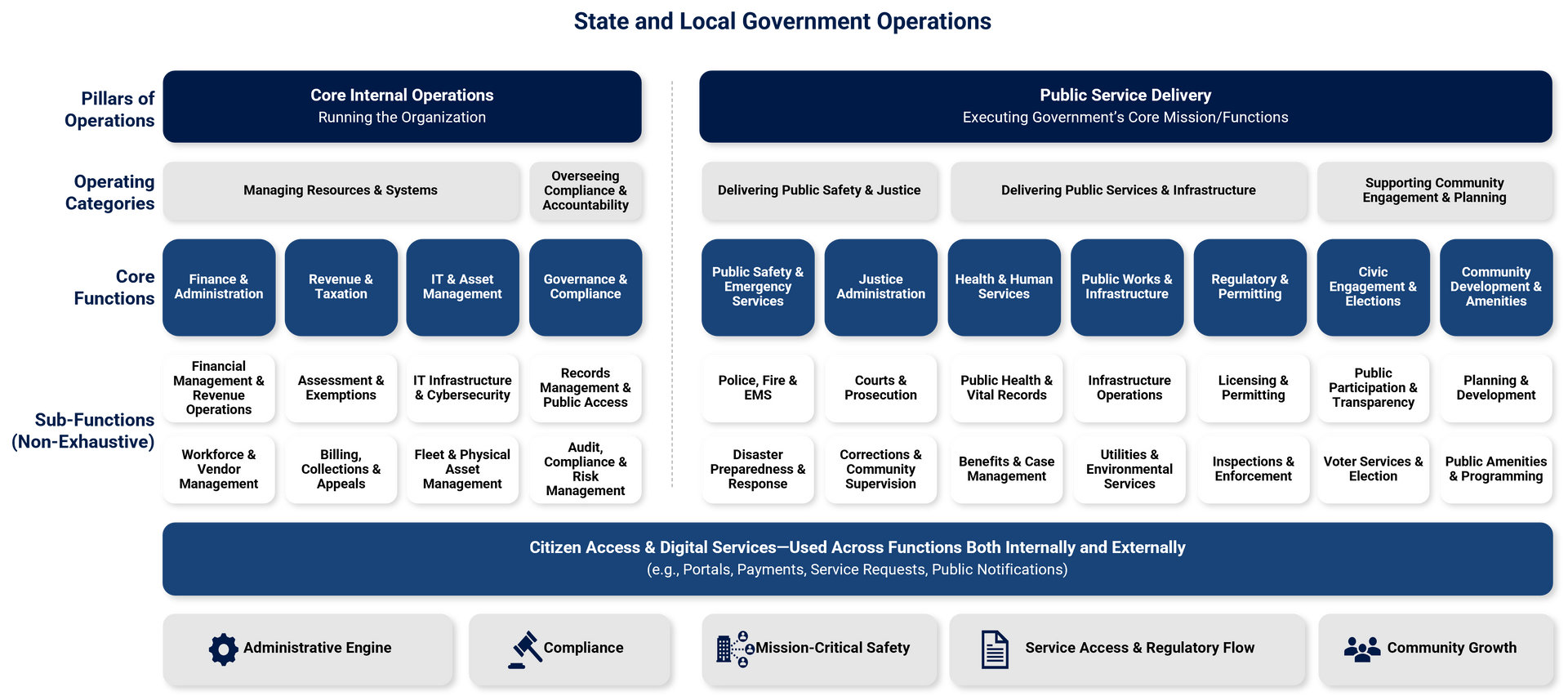

The GovTech ecosystem is complex, spanning a wide range of functions and serving many different state and local government (SLG) entities. At a high level, the landscape can be segmented into two major pillars:

- Core internal operations: Software that helps governments operate, including finance and administration, revenue and taxation, IT, asset management, and compliance.

- Public service delivery: Software that supports the government entities’ mission and core function. Examples here include public safety, justice administration, health and human services, public works, permitting, and civic engagement.

Overlaying both is a connective layer of software that enables citizen access and digital services across functions—portals, payments, service requests, and public notifications.

What makes the GovTech landscape unique is not just its breadth, but also the purchasing dynamics:

- Siloed decision-making across agencies and special districts: Purchasing authority for GovTech software typically sits at the department level (e.g., police, courts, finance) and is sometimes further fragmented into special districts that oversee specific functions (e.g., utilities, school districts).

- Highly localized requirements: GovTech software often needs to meet strict state and jurisdiction-specific regulations, workflows, and reporting standards. A solution that works well in one state may require meaningful customization to match the needs of another, making national scaling more challenging.

- High importance on trust and referencability: Government buyers heavily weight peer validation and proven track records of working with similar government entities. Vendors often need strong local / regional references to drive adoption.

The result of these factors is a market that has many vertical-specific point solutions and where competitive dynamics are often local or regional. GovTech is best considered as a collection of sub-verticals rather than a monolithic software category.

Market Trends

Across this fragmented landscape, several structural trends are driving demand and reinforcing the attractiveness of the category.

- Citizen expectations are escalating: Citizens increasingly expect fast, intuitive, digital-first interactions with government, mirroring private-sector experiences. This is creating strong pressure for SLGs to digitize operations and adopt technology that improves service quality, responsiveness, and accessibility.

- Federal aid withdrawal creates service delivery gaps: The federal government is pulling back from programs and funding it historically supported—including the sunset of major Covid-era grants—creating service gaps and voids that SLGs must fill with fewer resources and increasing demand for technology that drives efficiency and cost-effective service delivery.

- Regulatory pressures continue to proliferate: SLGs face both longstanding and newly emerging compliance and regulatory pressures driven increasingly by state-level mandates focused on transparency, reporting accuracy, constituent accessibility, and broader public accountability.

- Data protection and AI emerge as strategic priorities: Governments are balancing expanding federal and state-level data privacy and governance mandates with the adoption of AI-enabled tools, while active federal and state debates on AI governance signal momentum but leave the regulatory path uncertain.

- Platform vendors accelerate consolidation to capture wallet share: Leading GovTech platforms are increasingly acquiring and integrating niche point solutions to broaden functionality across government use cases, unify data environments to strengthen security posture, and deepen customer entrenchment.

- Fragmentation of GovTech solutions persists among smaller government entities: Despite consolidation among GovTech vendors, SLGs remain highly fragmented in their decision-making. They are historically more common in larger governments but increasingly seen among smaller ones. At the same time, technology adoption prompts decisions to align by function, creating departmental silos, inconsistent priorities, and decentralized procurement.

Investment Perspectives

As a category, GovTech stands out because it tends to be sticky, resilient, and supported by durable tailwinds. Spending is tied less to discretionary budgets and more to the ongoing need to maintain essential services, meet regulatory requirements and improve constituent outcomes. Many products become deeply embedded in government workflows, often serving as systems of record or systems of action around sensitive, regulated, or operationally critical processes.

Relative to other vertical SaaS, this category also seems to be relatively insulated from near-term AI disruption risk. In many GovTech sub-segments, there is minimal insourcing risk, limited horizontal player appetite, and decision-makers prioritize domain expertise, reliability, and compliance over adopting the newest technologies.

Within this context, we see two distinct investment themes worth highlighting:

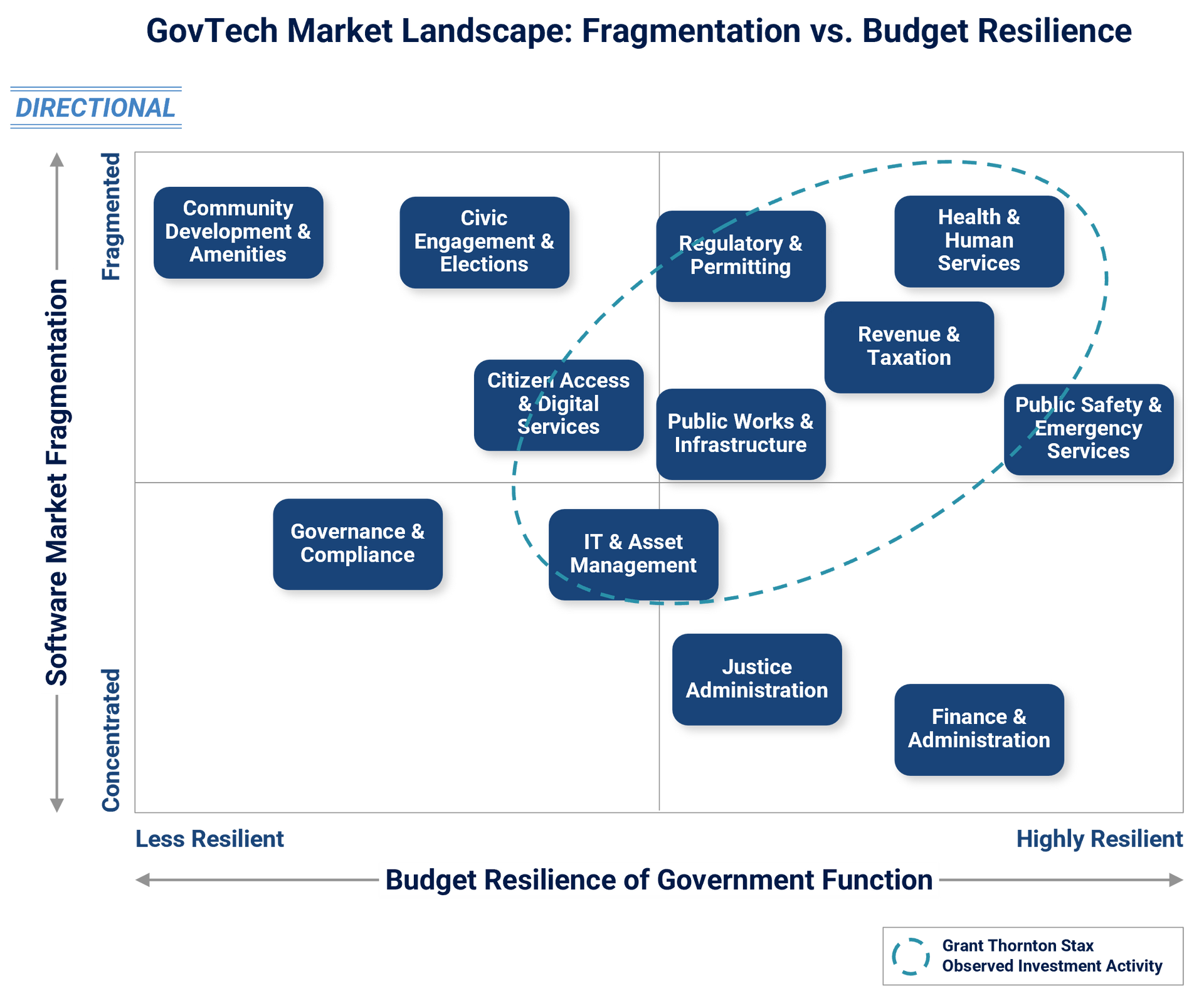

One potential opportunity in GovTech is to target sub-verticals that combine high fragmentation with budget resilience. In these markets – such as tax administration and permitting – investors can pursue roll-up or expansion strategies that create value through product-breadth, cross-sell, and improved go-to-market leverage. This is especially compelling for solutions that target mission-critical functions for state and local government entities, where durable budgets drive a clear path for platform consolidation.

However, investors need to be deliberate about which products belong together and where geographic nuance matters. State and local government requirements are rarely uniform. As a result, product-market fit in one state does not translate to another. Successful consolidation strategies require a real view on workflow adjacencies, buyer needs, and where the offering will have a strong right to win across geographies.

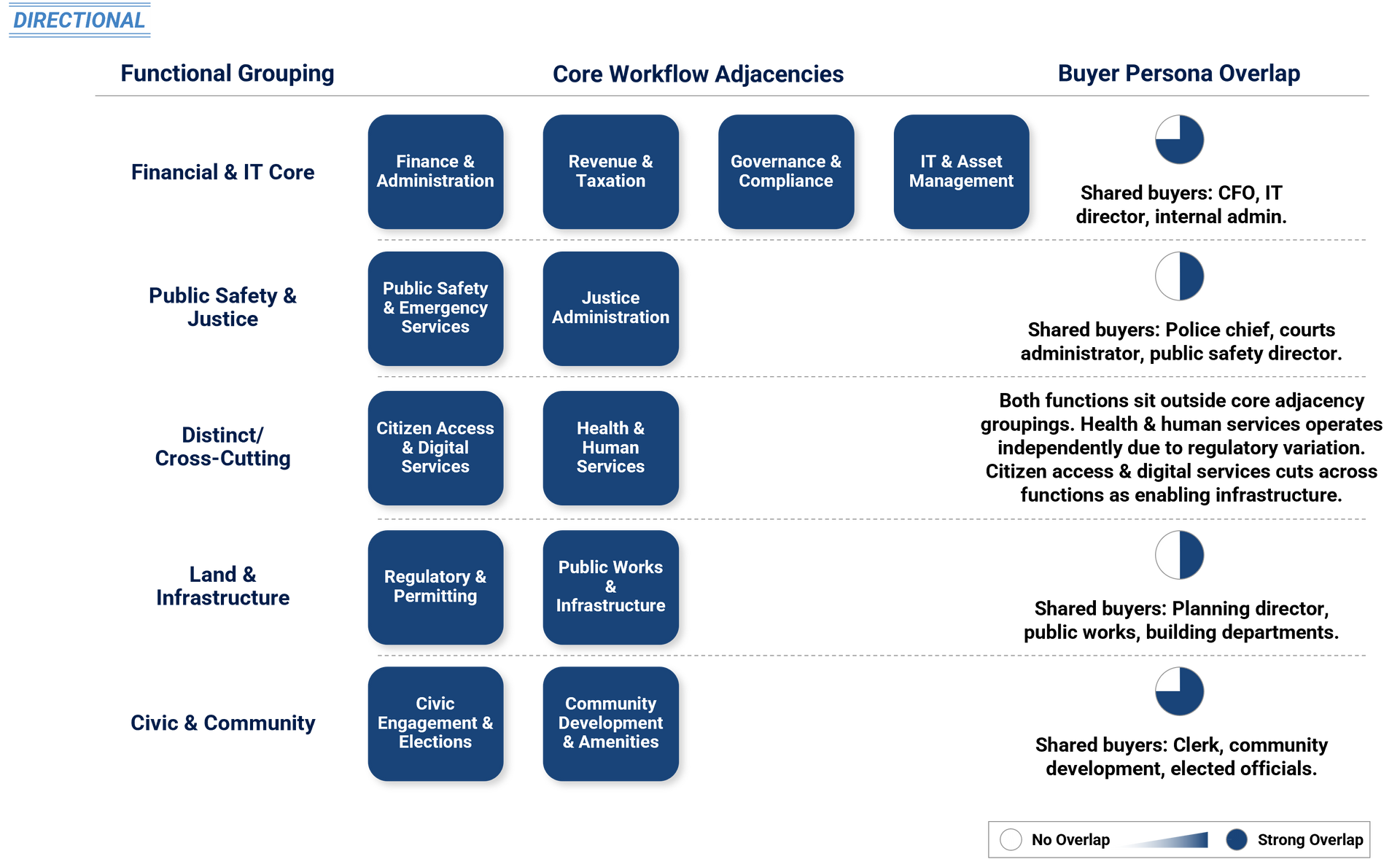

Another strategy we see in this ecosystem is the formation of platforms around shared functional groups where decision-maker overlap is meaningful and there is strong industrial logic. As government entities modernize and adopt additional software solutions, they are increasingly frustrated by the need to use multiple solutions that do not speak well with one another. Investors can create value by forming an integrated solution across products that naturally fit into adjacent workflows and have the same user and buyer personas.

However, a platform thesis only works well if the solutions are aligned. Decision-makers have become skeptical of the promise of a unified software platform that ends up being a collection of disconnected products. Emphasis should be placed on creating real workflow continuity with back-end data connectivity.

Conclusion

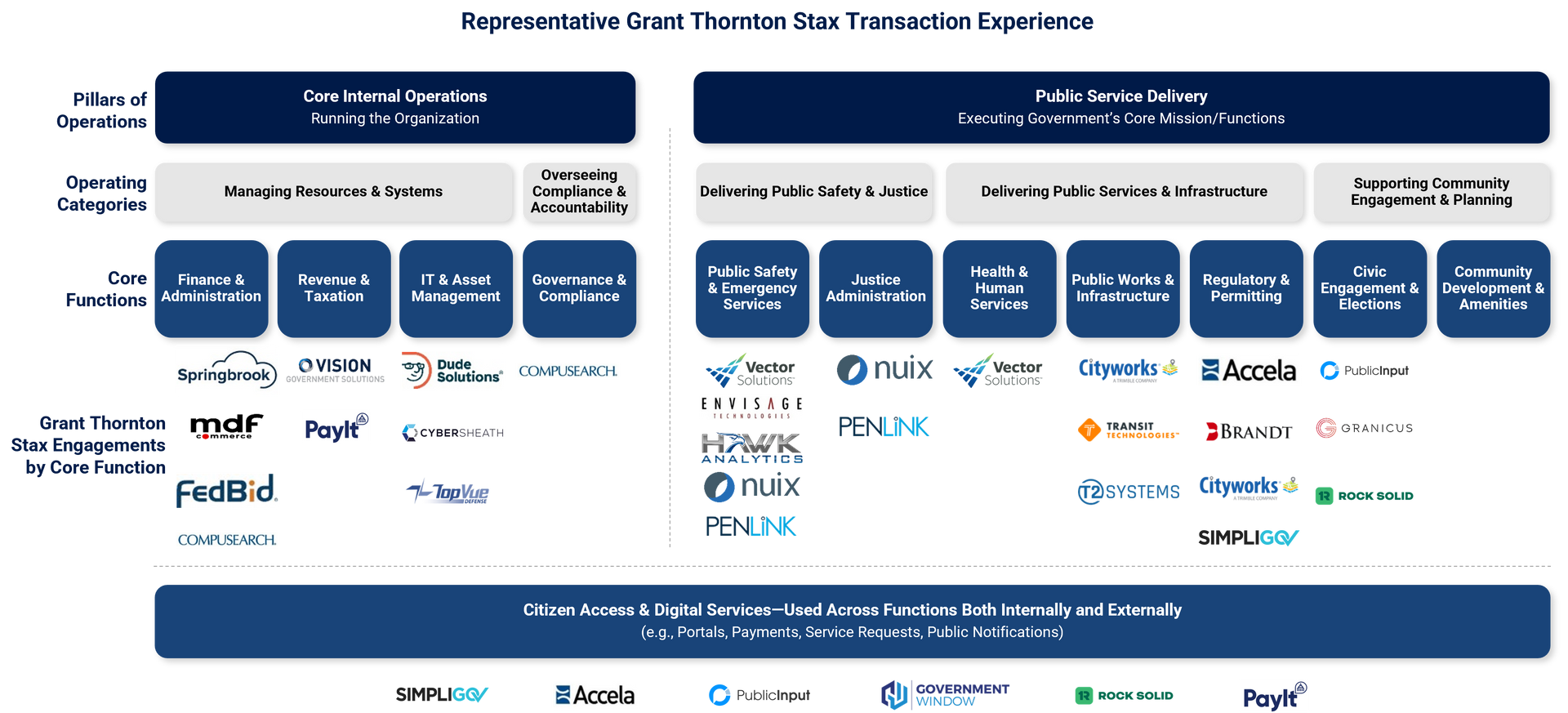

Our experience across the GovTech ecosystem reinforces this platform-driven investment thesis, with deep transaction exposure spanning civic engagement, payments, ERP, and tax administration systems. We have supported strategic buyers in identifying and underwriting cross-sell synergies within legislative and citizen engagement platforms, while also validating the ability of payment and workflow solutions to consolidate fragmented municipal systems. To learn more about our expertise, visit our Insights page or click here to contact us directly.

Read More