Share

Executive Summary:

The investigation management and digital intelligence software market is consolidating at the top, with well-capitalized platforms racing to own the full investigative workflow. The real opportunity for middle-market private equity is not in creating a replica of those platforms, but in identifying focused, mission-critical assets that serve specific buyer segments, workflows, or compliance environments the platform players have not yet reached. With purpose-built solutions still representing a small fraction of overall spend, and demand driven by structural rather than cyclical factors, this is a category where disciplined smaller-scale investment theses can generate compelling returns without requiring a platform arms race.

Why the consolidation playing out at the top of the market creates distinct opportunity—not crowding out—for middle-market investors.

A Large Market, Still Mostly Unserved

The digital forensics and digital intelligence software market is multi-billion globally, growing at double-digit rates. Within the US, the addressable universe spans roughly 15,000 state and local public sector law enforcement agencies, dozens of federal government agencies with investigative functions, and a private sector increasingly contending with fraud, misconduct, and regulatory scrutiny.

Despite this scale, most organizations still manage investigations on legacy government ERP systems, records management platforms not designed for investigative workflows, or spreadsheets. Purpose-built investigation management solutions currently address a small portion of organizations that could meaningfully benefit from them.

For middle-market PE, this creates a specific kind of opportunity: assets that are early in their penetration of a large, clearly defined market segment, not because the product is unproven, but because the buyer has not yet modernized.

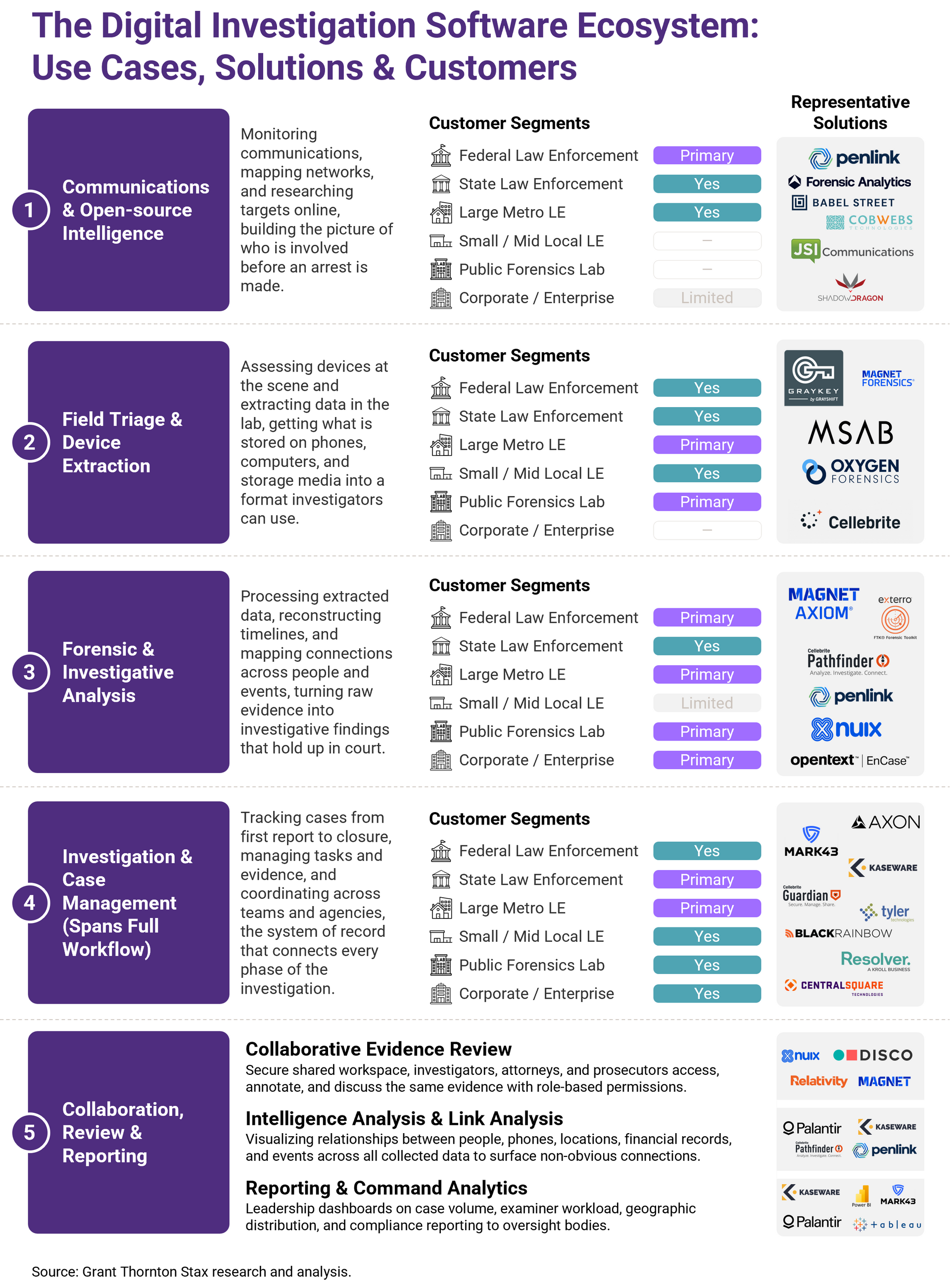

One Workflow, Two Distinct Phases

Before evaluating assets in this space, investors need to understand how the investigative workflow is structured, as vendors participate in different states of the process. Their position within the workflow determines competitive exposure, buyer relationships, growth potential, and ultimately enterprise value.

Every investigation moves through two phases, each triggered by a different legal event and drawing on a different method of data acquisition.

- The first is digital intelligence: this work typically happens before or during an active investigation, under legal authorities like wiretap orders or national security letters, with the goal of developing leads, mapping networks, and building probable cause. During this phase, collecting and analyzing data from external sources, lawful intercept of live communications, Open-Source Intelligence (OSINT) scraped from the open and dark web, subpoenaed call detail records and financial data.

- The second type of work is digital forensics: Usually follows an arrest or search warrant, under different legal standards, with chain-of-custody and court-admissibility as the primary requirements. Here, extracting and analyzing data from devices or systems the agency already has physical custody of, a seized phone, a confiscated laptop, a cloned hard drive.

These two phases are distinct enough that specialized vendors have built deep expertise and compliance infrastructure in each, the legal authorization that triggers the work is different, the technical architecture required is different, and within larger agencies the buyer persona is often different (intelligence analysts vs. forensic examiners).

But they are not fully separate: the output of both phases feeds the same investigation file, and at smaller agencies the same detective often does both. That overlap is precisely what is driving demand for unified platforms, not that the two functions are identical, but that the handoff between them is expensive when it requires switching systems.

Investigation case management sits above both phases as the connective tissue, the system of record that tracks what intelligence has been developed, what forensic analysis has been done, what evidence has been collected, and where the case stands. It is the least glamorous part of the stack and the most deeply embedded in daily operations.

Why Platform Consolidation Creates, Not Closes, MM PE Opportunity

The strategic logic of platform consolidation is sound, and the large players: Cellebrite, the combined Magnet/Grayshift entity, Motorola Solutions, Axon, are investing accordingly. But platform consolidation rarely means platform homogeneity, and this market has structural features that protect well-positioned focused assets.

- Procurement is fragmented. There is no single mandate governing how law enforcement agencies buy investigation software. State and local agencies, the largest segment by organization count, make purchasing decisions independently, through long sales cycles and multi-year contracts. A mid-sized department evaluating case management software is choosing from the handful of vendors that have cleared relevant compliance requirements and earned references in their geography, not selecting from a national shortlist.

- Compliance credentials are a genuine moat. CJIS security standards, FedRAMP authorization, and StateRAMP certification are not marketing checkboxes. They involve independent audits, data residency constraints, and ongoing maintenance. Vendors who have earned these credentials hold a competitive advantage that protects customer relationships regardless of relative product sophistication while also keeping out larger competitors who have not made the same investment in a given segment.

- Use case depth beats breadth at the margin. Platform players optimize for the broadest common denominator. Assets that have built deep workflows for specific buyer segments—Offices of Inspector General, mid-sized metropolitan departments, enterprise fraud teams—can maintain strong competitive positioning in those segments even as broader consolidation unfolds around them.

What Middle Market PE Should Be Looking For

A few principles consistently differentiate assets that perform from those that plateau:

Workflow depth beats feature breadth

The most defensible assets have become genuine systems of record, platforms so embedded in daily operations that replacement requires retraining staff, migrating complex case histories, and re-establishing compliance certifications. This shows up in net revenue retention and the nature of competitive evaluations at renewal, not in product comparison matrices.

The displacement thesis needs a specific mechanism

The observation that most of the market is still utilizing legacy tools is necessary but not sufficient. The questions are what specifically will cause buyers in the target segment to modernize, on what timeline, and whether this asset wins that displacement. Federal grant programs funding technology modernization, court cases creating pressure to upgrade evidence management practices, state-level incident reporting mandates, these are the kinds of catalysts that turn secular tailwinds into executable theses.

Private sector crossover is underexplored optionality

Many vendors in this space have built their customer base entirely in the public sector and have not seriously evaluated the enterprise opportunity. Large enterprises face rising volumes of internal investigations driven by fraud, misconduct, and regulatory scrutiny, and the underlying workflow is structurally similar to the public sector. For the right asset, that represents genuine TAM expansion that is not yet priced in.

AI Is Expanding the Market, Not Disrupting It

The relevant framing for AI in this space is not disruption but expansion. Investigations suffer from a data volume problem, not a data scarcity problem, and AI directly addresses it through:

- Pattern recognition across large datasets

- Automated entity extraction

- Anomaly detection in financial records and communications data

- Natural language interfaces that make complex tools accessible to non-specialist users

For software platforms, this creates a seat expansion opportunity. In the past, investigation tools typically required trained forensic analysts or experienced investigators to operate. AI-enabled interfaces lower that barrier enough to extend platform value to patrol officers, HR teams, compliance officers, and fraud analysts—users who would not previously have been licensed on the platform. This is revenue growth within existing customer organizations that does not require proportional increases in sales investment.

The AI transition also favors incumbents with strong data positions. Vendors who have accumulated large, well-structured investigative datasets have a training advantage that newer entrants cannot easily replicate—which means well-positioned smaller assets have more runway through the AI transition than a purely product-capability comparison might suggest.

Conclusion

The investigation management software market is a genuine middle market PE opportunity, not because it is undiscovered, but because the consolidation at the platform level is clarifying which buyer segments, workflow layers, and compliance niches remain the territory of focused assets that are not trying to be Cellebrite.

Demand is structural and growing. The vended market is a small fraction of the total opportunity. Switching costs in established customer relationships are real. And AI is expanding the addressable user base within existing customers in ways that drive seat-count growth without proportional sales investment.

The firms that will generate the strongest returns will identify assets with genuine workflow depth in a well-defined buyer segment, validate the displacement thesis with specific catalysts, and build the compliance infrastructure that converts individual customer relationships into defensible market positions.

To learn more about our work in investigation management, digital intelligence, and government technology software, visit our Insights page or contact us directly.

Read More